Annualization of Returns

Contents

Returns are only annualized when the holding period is longer than 11 months. This prevents distortion of returns, yet allows for annualization for periods of slightly less than a year.

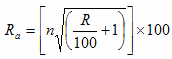

The formula used is:

where n is the number of years in the period and R is the return for that period.